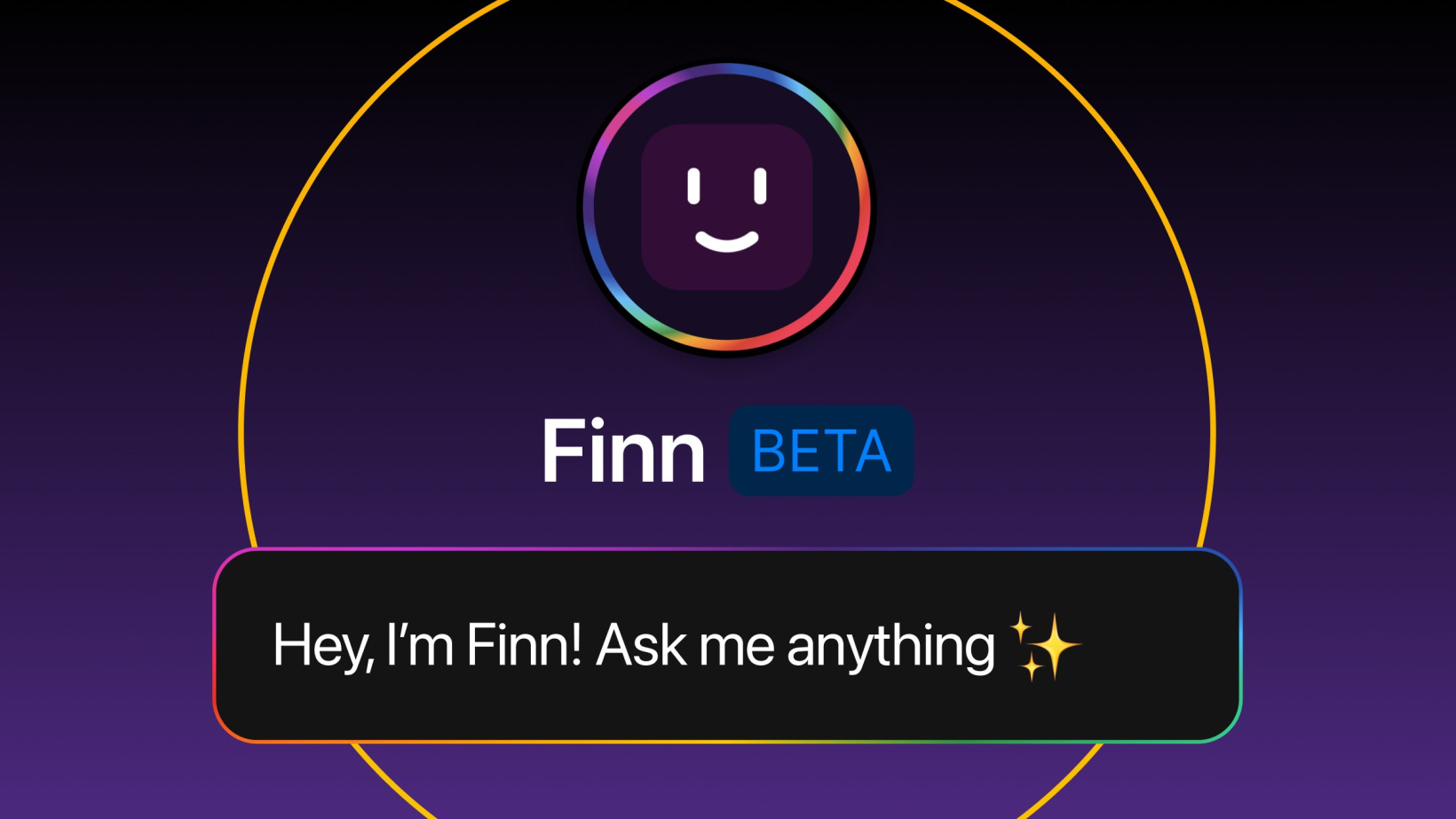

Nowadays, Dutch neobank bunq introduced its generative AI platform — Finn. Working on open massive language fashions (LLMs) from OpenAI and Meta, the brand new chatbot serve as is designed to assist customers plan their price range, make higher budgets, and simply in finding transactions. Necessarily, consistent with bunq, enabling customers to “are living the existence they would like.”

“It’s principally as you probably have your individual private accountant who is aware of the whole thing about your own existence, and about your transactions, and has all of this of their head and will solution no matter questions you’ve,” Ali Niknam, bunq’s founder and CEO tells TNW.

Whilst the brand new AI chatbot interface will substitute the quest serve as at the bunq app, Niknam is raring to spotlight that Finn is a lot more than only a seek bot. The use of the LLMs discussed above (Gemini may just see an integration down the street), having made up our minds which gives the simpler solution, bunq has created its personal type that may interpret and develop into what a person is looking. This permits for solutions which might be “way more advanced” than an ordinary seek question.

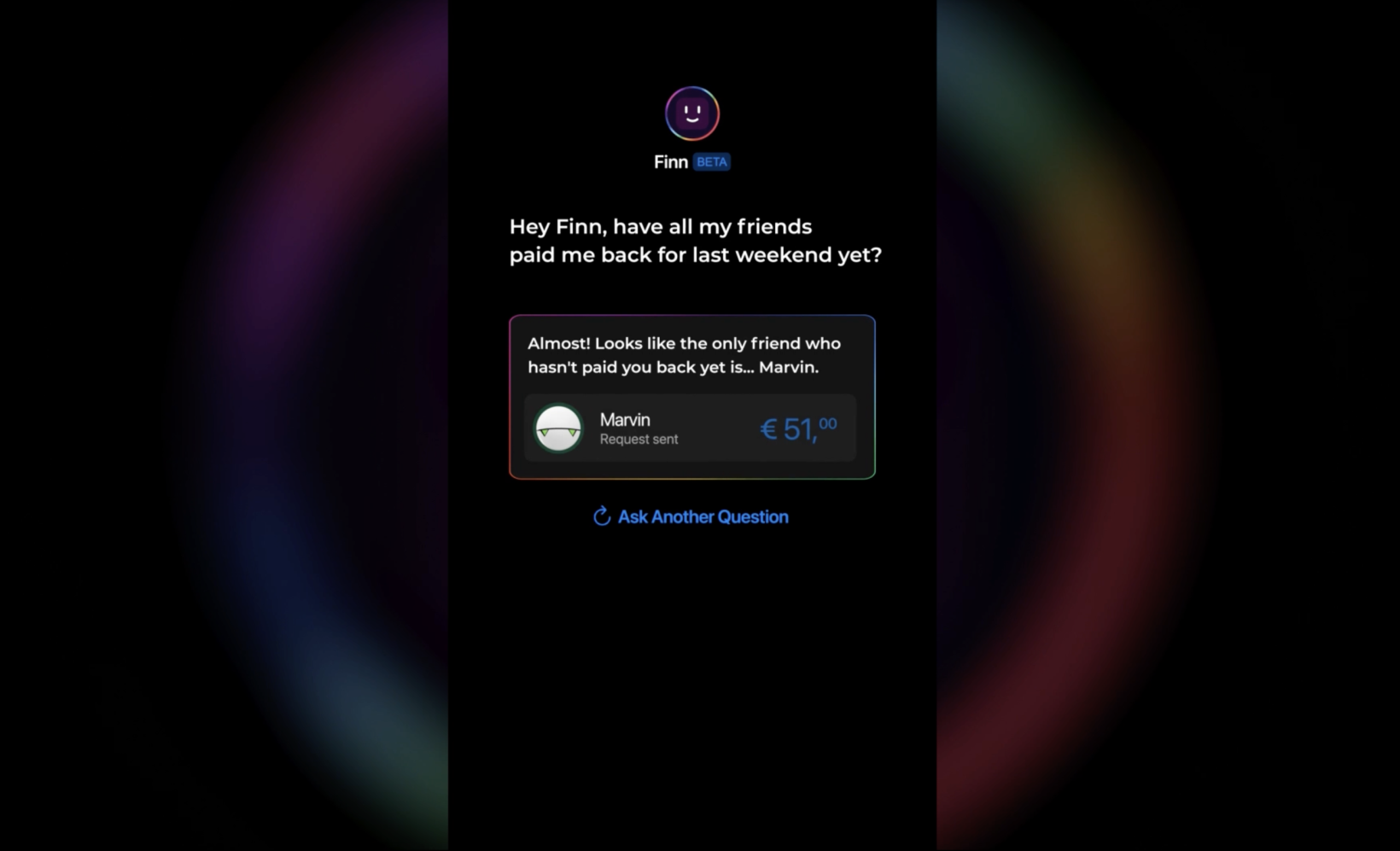

“Finn can in fact give that means to the entire knowledge that you’ve generated by means of doing all your transactions. So you’ll be able to ask cool stuff like, whats up, what’s my favorite eating place within sight?” Niknam says.

Finn will really feel acquainted to any person who has used an LLM person interface similar to ChatGPT, or impartial seek engine Ecosia’s new ‘inexperienced’ chatbot. Different instance activates might be such things as “how a lot did I spend on Amazon this 12 months” or “what used to be the identify of that resort I stayed in Berlin remaining April.”

It might probably additionally inform customers their particular spending patterns, assist them finances for an upcoming commute, and inform them precisely when a purchase order used to be made — with no need to scroll endlessly whilst racking one’s mind for approximate dates (or is that simply us?).

Will legacy banks release their very own AI chatbots in reaction?

Niknam, born in Canada to Iranian folks and raised in Gouda, the Netherlands, based bunq in 2012. Two years later, the fintech startup was the primary financial institution to get a Eu banking licence in 35 years. It reached unicorn standing in 2021, and is the second one greatest neobank in Europe. The United Kingdom’s Revolut is the biggest (bunq needed to forestall accepting new purchasers in the United Kingdom after Brexit).

When bunq introduced to the general public in 2015, it compelled legacy banks to up their app sport — which used to be up to now lovely appalling. May just the discharge of Finn spark a equivalent rush of GenAI purposes for the massive banks? In line with Niknam, that may be a tricky query to reply to.

“For competent AI other folks, it’s not that tricky [to build an LLM chatbot], however to make one thing this is excellent, and to make one thing that may solution questions which might be extra insightful, extra clever, than just getting a host of transactions and including them in combination — this is very sophisticated,” he states.

“As a result of for you in an effort to do this, you wish to have to have the garage of your knowledge so as. And plenty of of those legacy banks have best been ready to stay alongside of the entire app tendencies by means of development a layer on best.”

“So possibly, I wouldn’t be stunned if we get one thing in numerous months. However I might be very stunned if we get anything else helpful within the upcoming years,” he provides.

The advantages of being a neobank on the subject of knowledge

It will take a little time for Europe’s neobanks to earn the similar family popularity as main banks that may hint their historical past again masses of years. On the other hand, on the subject of tech — and serving a tech-savvy era — being the brand new child at the block has particular benefits.

“We had been running with AI a very long time ahead of we added gadget studying fashions,” Niknam says. “So we’re manner forward of these items. And since we’re so engineering and AI centered, we made positive from the start of bunq that our knowledge buildings are helpful and usable by means of AI other folks. And we’re reaping the result of that.”

In all honesty, we’re moderately intrigued to look if Finn will make maintaining a tally of private price range extra amusing. Within the interim, we (along side a couple of different Amsterdammers) will likely be asking Finn “how a lot did I spend on pastry and oat flat whites in 2023” with gentle trepidation.

How Finn were given its identify? Why, bunq requested ChatGPT “what must we name our app’s private finance copilot,” in fact.

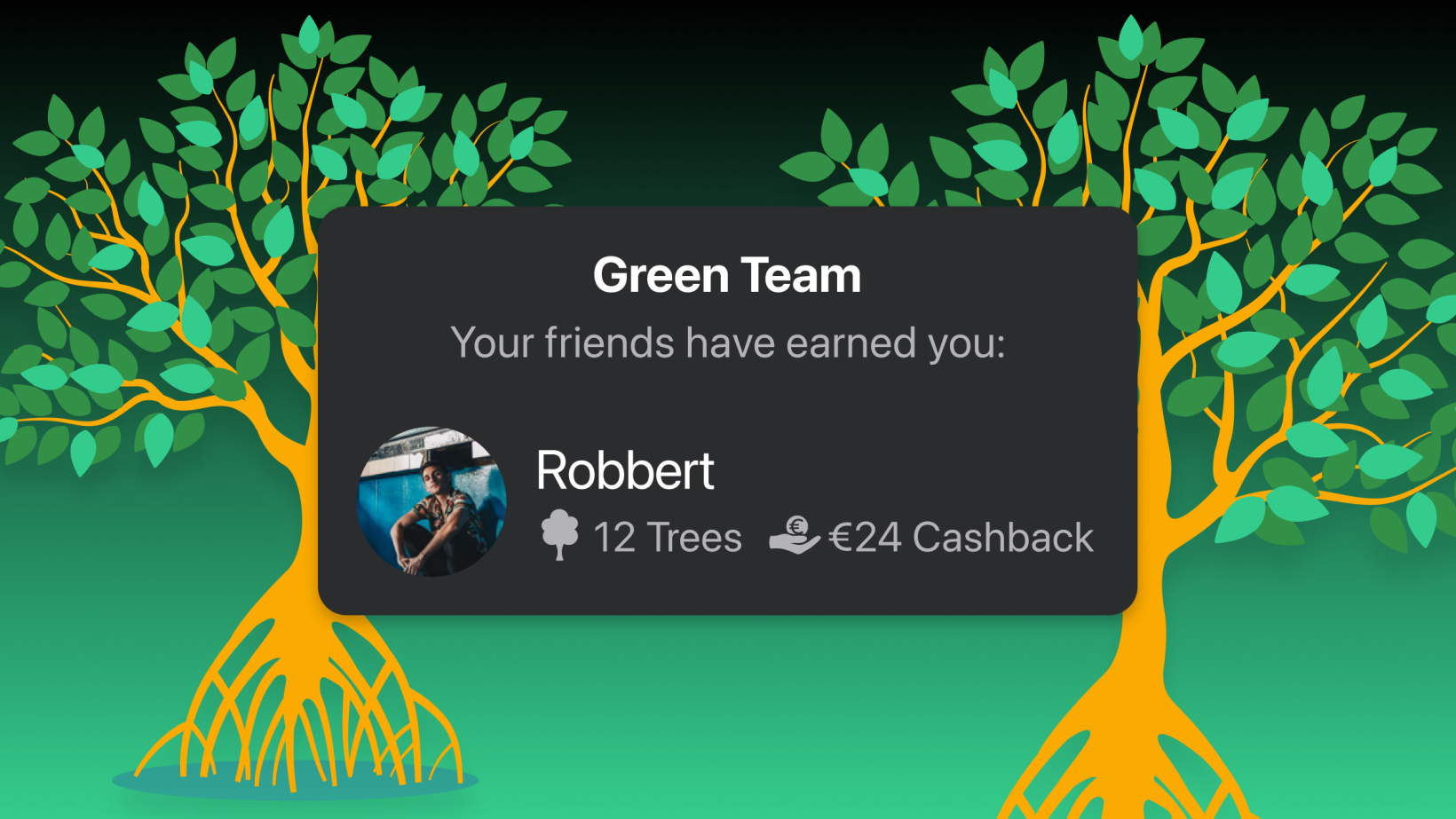

The corporate additionally introduced a number of new options at its once a year replace match. Those come with a brand new budgeting tab that permits you to set spending limits and come to a decision from which account the fee for particular pieces will likely be made, double money again for other folks in the similar tree-planting “inexperienced group,” unfastened bank cards, and tap-to-pay at the telephone for trade customers.